Key takeaways:

- Increasing the percentage of equity / stocks in your portfolio is a near sure fire way to increase the long term returns from your portfolio

- But increasing equity / stocks also makes your portfolio much more volatile in the short term

- Risk & return are two sides of the same coin. You can’t have one without also getting a fair share of the other 😊 More equity allocation = More risk = More return

- Looking at some of the worst market crashes in Indian market history, one should ideally be prepared for a 50 to 60% fall in the equity portion of one’s portfolio and be prepared to hold onto those investments for 5 years

- In addition to many other methods, Dr. Bernstein has a simple method that can help you decide what stock allocation would work for you based on your loss tolerance

- You can check the equity allocation of your portfolio by creating a free account on Kuvera or valueresearch

Primary determinant of long-term wealth

One of the primary factors that determine long-term wealth when investing in equity is the percentage of stocks / equity that you decide to have in your portfolio. The higher this percentage the more likely you will end up wealthier long term. However, there is corresponding risk. And it is this risk that many tend to gloss over or ignore when deciding on their asset allocation. I would urge everyone to very carefully consider the risk when deciding on how much money to put into stocks / equity mutual funds.

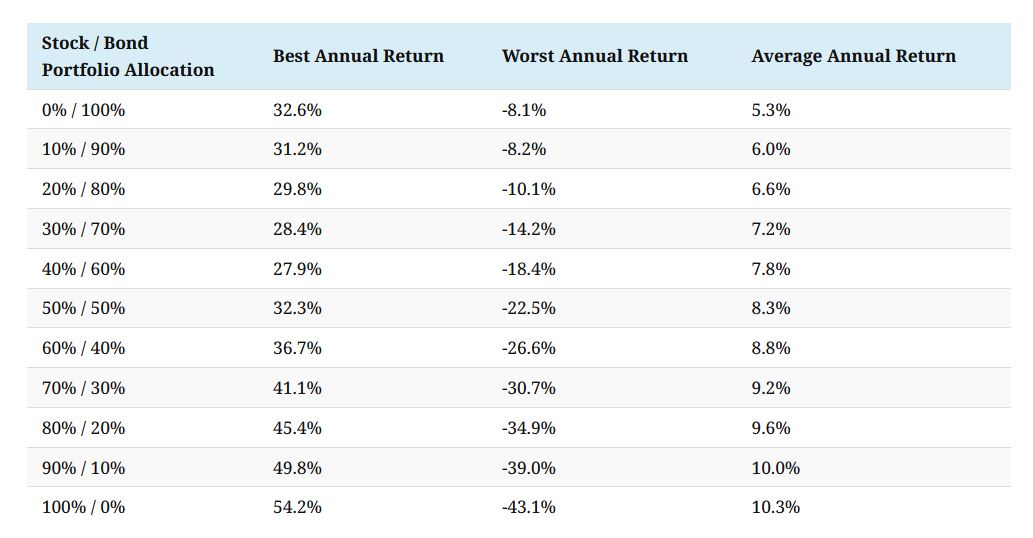

Correlation between percentage of equity & returns

The data below is from Vanguard and is based on US stock market data from 1926 to 2019. Although this is data based on the US market history, I include it here as a starting point since looking at market history over nearly 100 years is illustrative of the general correlation between asset allocation, returns & risk. Also, we have relatively less history on Indian stock markets.

The data below shows clearly how returns increase as you increase the percentage of equity in your portfolio.

As an example, let’s take an 80 / 20 stock vs bond allocation. (third last row from the bottom of the table above). You can see that for this aggressive allocation the average annual return is 9.6%. i.e. high stock allocation = high return. However, look at how wildly the annual returns fluctuate. From minus 34.9% to plus 45.4%. That’s the kind of annual volatility one needs to be prepared for.

Risk & return are therefore two sides of the same coin. You can’t have one without also getting a fair share of the other 😊 More equity allocation = More risk = More return

Some of the worst crashes in Indian stock market history

Let us now look at data from Indian stock market history to get a feel for what the worst crashes have looked like.

The chart below shows how much the Sensex fell during the 2008 crash. You can see it went from 20,873 to 8,160 which is a 61 % decline

While this is indeed a worst-case scenario that doesn’t happen often one does need to be prepared for it not just financially but emotionally & mentally as well 😊

The second steepest decline in the stock market was during the dot com crash between the years 2000 and 2001. As you can see from the chart below the Sensex fell from 5933 to 2600. That’s a 56% fall from it’s peak.

Typical times taken for stock prices to recover from crashes

As we have seen above, the first kind of risk you need to be able to bear when investing in the stock market are the extreme crash scenarios. This is why, you should probably never count on the returns from stock market linked investments to pay for any non-negotiable monthly expenses like say school fees or other monthly bills.

But apart from the wild swings in annual returns, you also need to be able to hold on to investments when they have fallen. How long should you be able to hold on? Let’s look at the data below on how long it has typically taken for stocks in India to recover from falls.

Notice that in the worst case, it took nearly 5 years for the stock markets to recover after the 2008 financial crisis.

So just as the percentage of stocks in your portfolio is a primary determinant of RETURNS, it is equally a primary measure of RISK (or rather volatility) in your portfolio

As in all things in life, one needs a balance. Keep increasing the percentage of equity / stocks without restraint and you could end up in serious trouble. And so, we need debt or bond investments in good measure for balance.

From the above historical data on the worst crashes in Indian stock market history, you can see that as an approximation, you need to be able to handle a 50 to 60% fall in the value of your stock or equity investments and be able to hold on to it without selling for 3 to 5 years.

Dr. Bernstein’s loss-tolerance based asset allocation approach

It is based on this principle that Dr, William Bernstein recommends using the following table as a simple guide to deciding what percentage of your portfolio you should have in stocks / equity. (i.e. volatile / risky assets)

The column on the left indicates how much of an overall loss (temporary say up to 5 years) in your portfolio you feel you can comfortably handle

As an example, I currently have approx. 30% invested in equity. Looking at Dr. Bernstein’s table above, I note that I should be prepared for a 10% overall loss in my portfolio and I should have the financial ability as well as mental & emotional tenacity to hang onto that loss for about 5 years

Action: Check what is the percentage of equity / stocks in your portfolio as per the steps outlined below. Then look at the row in Dr. Bernstein’s table above with the percentage of stocks / equity you found that you have in your portfolio and assess whether you can tolerate a portfolio loss equal to the corresponding value in the column to the left.

How to check your stock vs bond OR equity vs debt allocation

Follow the steps below to create a free account on Kuvera & upload your investments into it. From your Dashboard view, scroll down and click on “Portfolio Analytics”. There your equity vs debt allocation is clearly visible on the dashboard something like this.

Step 1: Create an account on Kuvera

Step 2: Import all your mutual funds into Kuvera

Step 3: View your portfolio analytics

Alternately, here’s an article from Valueresearchonline that helps guide you on what you need to do to get all your investments imported into the tool. It’s super simple, easy & convenient. If you have any trouble doing this, drop me a direct message and I can help.

Disclaimer: I am not a financial advisor. My articles are meant for people who are not savvy or well versed with personal finance and investing and find it difficult to grasp all the jargon typically used when discussing such topics. I hope to be able to demystify investing and make it as simple as possible for everyone. I’ve invested in Mutual funds for approx. 24 years. I’ve also been a diligent student of the subject of investing over the past 24 years learning & applying the writings of luminaries in the field. In these articles I’m merely sharing my experience & learning from that investing journey and the books of luminaries in the field in the hope that it might help others in some way. I am in no way directly or indirectly claiming to be a hot shot investor who has generated exceptional or even above average returns during my investment journey. However, I am quite confident that even if all you do is learn from my mistakes, educate yourself on sound investment principles & develop good financial habits you will benefit greatly. Please ensure that you consult a financial advisor before taking any decisions or actions concerning your personal finances or investments. I shall not be liable.