Key takeaways

-

Comparing the returns of your Fund’s SIP vs an SIP in it’s corresponding Index is the most basic measure of performance

-

It’s critical that a fund beat it’s benchmark because most funds charge between 1% to 2% for the expertise of their fund management team to beat the Index

-

If your fund is not providing better returns than it’s corresponding Index, then you are effectively giving up between 1% & 2% of your investment returns for nothing.

-

Even a 1% fee becomes very significant over decades of investing. e.g. it can reduce 20% of one’s retirement income, or 26% of one’s net worth

-

In almost all portfolios I have reviewed, more than half the funds don’t beat their Index

-

I’ve outlined below the simple steps you can take to do this comparison yourself

-

If you would like me to do a similar review, reach out & I’d be happy to discuss

If you want to know how well (or not) your fund is performing, the most basic test is to benchmark it’s returns against IT’S CORRESPONDING INDEX.*

The above performance check is the equivalent of getting a Pass or Fail on your report card at school or college. Yet, very few investors do this simple yet most fundamental check while reviewing their portfolios.

I’ll be honest. Even I didn’t do this for a long while. Why? Laziness. It takes a fair bit of effort & time to do it. Hardly any investment advisor or tool today gives you such a report. (If you know of one, please message me & let me know) So it’s up to us to do it ourselves. I would much rather look at a ready made report that someone in the investment industry hands me & just review the numbers they were showing me.

Why compare your fund performance to it’s corresponding benchmark index?

A mutual fund manager is expected to use his / her skills & judgement to pick stocks and provide you with better returns than a known set of companies in the corresponding benchmark Index. It is mainly for this potential SKILL of a fund manager that the Total Expense Ratio of between 1.5 to 2% is charged to you as an investor.

If your fund is not providing better returns than it’s corresponding Index, then you are effectively giving up 1.5 to 2% of your investment returns for nothing. You could easily just pick an broad based market cap weighted Index fund (not ANY Index fund) directly yourself without any professional stock picking skills on your part.

The massive impact of fund fees

A couple of pointers below as to why even just a 1% fee which seems very negligible may not be so easily dismissed:

-

Nobel laureate William Sharpe’s take is that a 1% advisor fee can reduce retirement spending by 20%.

-

Here’s an excellent article by Investment Advisor Avinash Luthria in The Mint. His calculations seem to suggest 26% lower net worth over 30 years !

-

Lastly, here’s an article from Rob Berger, entitled “How investment fees affect wealth”. In the article he shows that fund fees can reduce a final retirement corpus down from $3.1 million to $1.7 million over 45 years

I had earlier written an article that shows a quick dipstick way to get a sense of whether a fund is beating it’s benchmark Index or not. This method can be used when deciding whether to invest in a fund or not. However, once you have invested in a fund & when you are reviewing it’s performance as part of your portfolio review, this method below is a more accurate (though not perfect) way to do that.

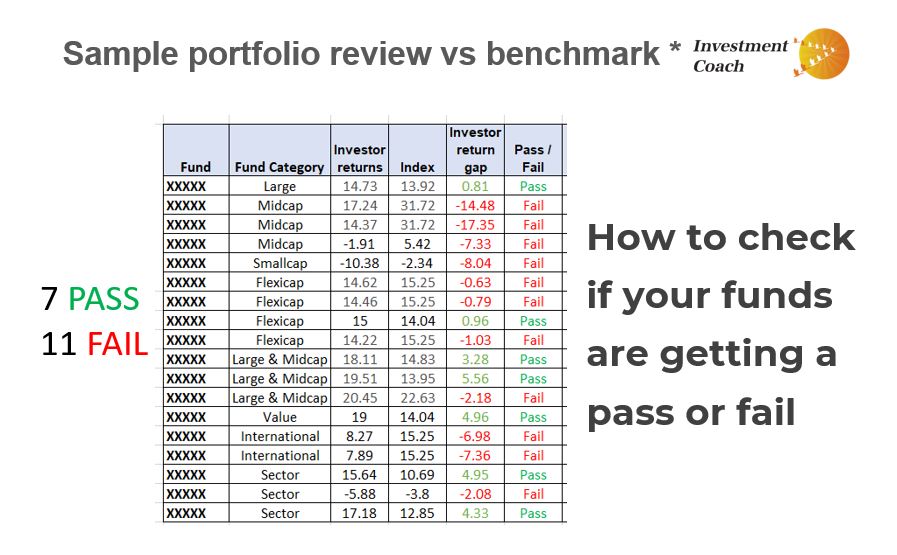

Just so you can get a feel for what the results look like, I’ve included a sample analysis of a real portfolio below:

If you would like me to do a similar review for your portfolio of funds, reach out & we can discuss.

How to ACCURATELY benchmark a fund’s returns vs it’s benchmark

There are fundamentally 3 important points to keep in mind as you start such a benchmarking exercise:

-

Choose the correct corresponding benchmark Index* based on the fund category

-

Compare returns for the same time period during which you invested

-

Ensure that your fund’s returns are calculated & reported as XIRR & not CAGR

Steps for fund performance benchmarking using an example

The example below is of an actual fund from an investor’s portfolio.

Step 1: Identify the correct benchmark Index

-

Search for Your Fund on Valueresearch: Google your mutual fund’s name along with the correct plan on valueresearch e.g. regular or direct (most people will be invested in the Regular plan) So I would do a google search like the following: “Mirae Asset Midcap Regular Valueresearch”

-

Click on the “Returns” tab on the fund’s page

-

Scroll down to the “Returns over time” table

-

Look for the Index in the 2nd row. In the example below the Benchmark Index for Mirae Asset Midcap fund is BSE 150 Midcap TRI

Step 2: Get the start date of your investment

-

Download the statement of your Mutual Fund since inception (you can get this from CAMS or KFintech or from the AMC’s website)

-

Look for the date on which your SIP started & note the date. For the sake of example, let’s say you started investing in the fund in 2020

Step 3: Get the returns of an Index fund for your years of investment

-

Next, we want to know the returns of the BSE 150 Midcap TRI for the period of your investment

-

Now we need to find a fund that mirrors the above Index. So we Google for “Index funds that track BSE 150 Midcap TRI” … and Motilal Oswal Nifty Midcap 150 Index fund shows up.

-

Next go to the fund page on Valueresearch for the above Index fund i.e. Motilal Oswal Nifty Midcap 150 Index fund

-

Go to the “Returns” tab of the fund

-

Scroll to the section at the bottom of the returns tab titled “Calculate SIP / SWP returns”

-

Enter zero in the “Upfront investment” field

-

Enter your SIP value or any dummy value into the field “Monthly SIP amount”

-

Enter the number of years you have held the investment. In this case since we are in 2026, I enter 6 years for the above example since the fund was bought in 2020

-

Then hit the “Calculate” button

-

You’ll see a return number like the one below showing 20.78 %

Step 4: Get your fund’s actual XIRR returns

-

Import your investments into Kuvera or any other app

-

Look at the XIRR returns shown in the app

If the returns from Step 4 are higher than what you got in Step 3, your fund is passing the exam. If not, it’s failing.

Note: I have intentionally capitalised & made bold the words “corresponding index” because many investors are often misled by people in the financial industry who seem to compare fund returns irrespective of fund category ONLY against the Nifty 50 Index or Sensex. This is an apples to oranges comparison & therefore completely wrong.2. Select an angle or point of view – Angle neither too broad or too narrow

Summary

From the portfolios I’ve reviewed so far, I’ve seen a consistent trend that shows that more than half the funds typically under perform their Index

If you would like me to do a similar review for your portfolio of funds, reach out & we can discuss.

Disclaimer: I am not a financial advisor. My articles are meant for people who are not savvy or well versed with personal finance and investing and find it difficult to grasp all the jargon typically used when discussing such topics. I hope to be able to demystify investing and make it as simple as possible for everyone. I’ve invested in Mutual funds for approx. 24 years. I’ve also been a diligent student of the subject of investing over the past 24 years learning & applying the writings of luminaries in the field. In these articles I’m merely sharing my experience & learning from that investing journey and the books of luminaries in the field in the hope that it might help others in some way. I am in no way directly or indirectly claiming to be a hot shot investor who has generated exceptional or even above average returns during my investment journey. However, I am quite confident that even if all you do is learn from my mistakes, educate yourself on sound investment principles & develop good financial habits you will benefit greatly. Please ensure that you consult a financial advisor before taking any decisions or actions concerning your personal finances or investments. I shall not be liable.