Key takeaways

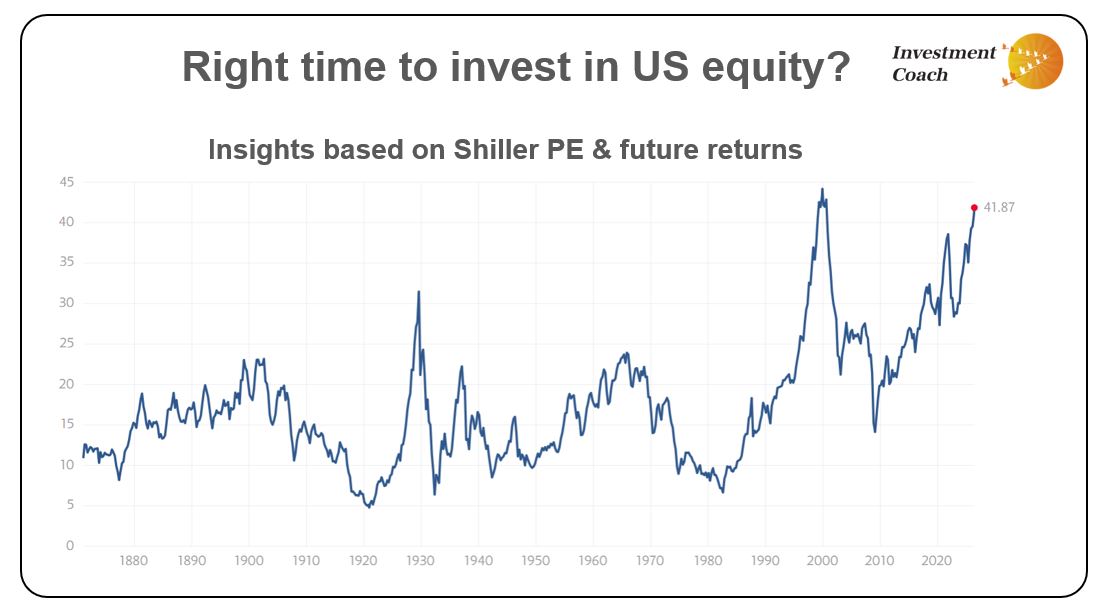

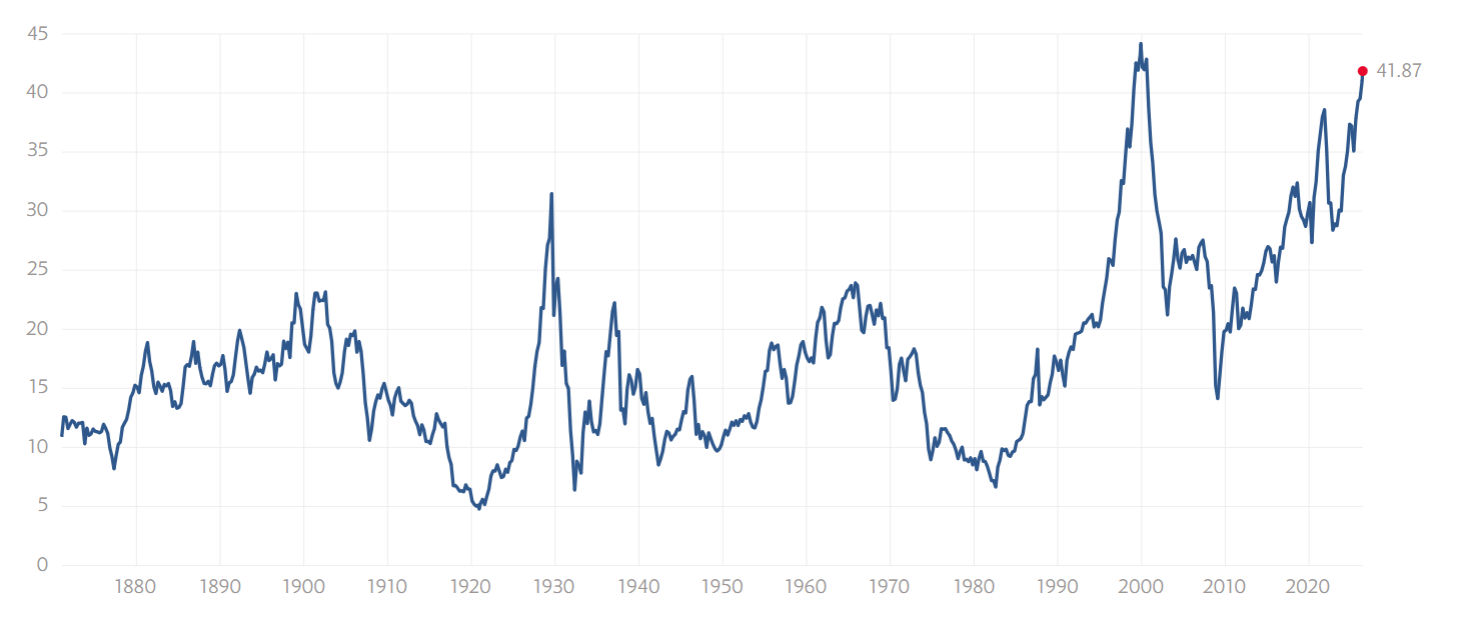

- The Shiller PE (CAPE) ratio of the US market is currently around 41.87 — the second-highest level recorded since 1880

- The only period with higher valuations was around the year 2000, just before the dot-com crash

- Historical data suggests that starting valuations and future 10-year returns tend to have an inverse relationship

- In simple terms: the higher the starting valuation, the lower the likely long-term returns

- At current Shiller PE levels, based on historical data, projected 10-year US equity returns may be very low

- Indian investors should also keep in mind that RBI overseas investment limits have reduced the availability of SIP-based investment options into international funds. Constrained choice means you might be forced into a fund that isn’t the best

- GIFT City structures provide another route for investing abroad, but many currently require relatively high minimum investments (often around ₹5 lakh), increasing the risk of investing a large lump sum at elevated valuations

Given the relatively lack luster performance of the Indian markets over the past 18+ months, a lot of investors seem to be looking to the US markets to diversify. Why? For most people, it’s because they’re looking to get better returns and the US markets have delivered stellar returns nearing 20% in recent years. So it’s natural to look to invest there,

However, if one does decide to invest in the US equity markets right now it’s important to invest with the right expectations of future returns. (at least from the perspective of the next 10 years) Why? Because this is what Buffett has described as driving by looking in the rear-view mirror. In short, what Buffet means by that is that past high returns do not necessarily mean high future returns. In fact, past high returns normally indicate muted future returns.

In particular, one does need to keep an eye on valuations when investing in any country or asset class.

Keeping an eye on Valuations

Below is a chart of the Shiller PE ratio of the US S&P 500 from 1880 till date

Notice that the Shiller PE is at it’s second highest valuation since the year 1880. The only time it’s been higher was around the year 2000 prior to the dot com crash.

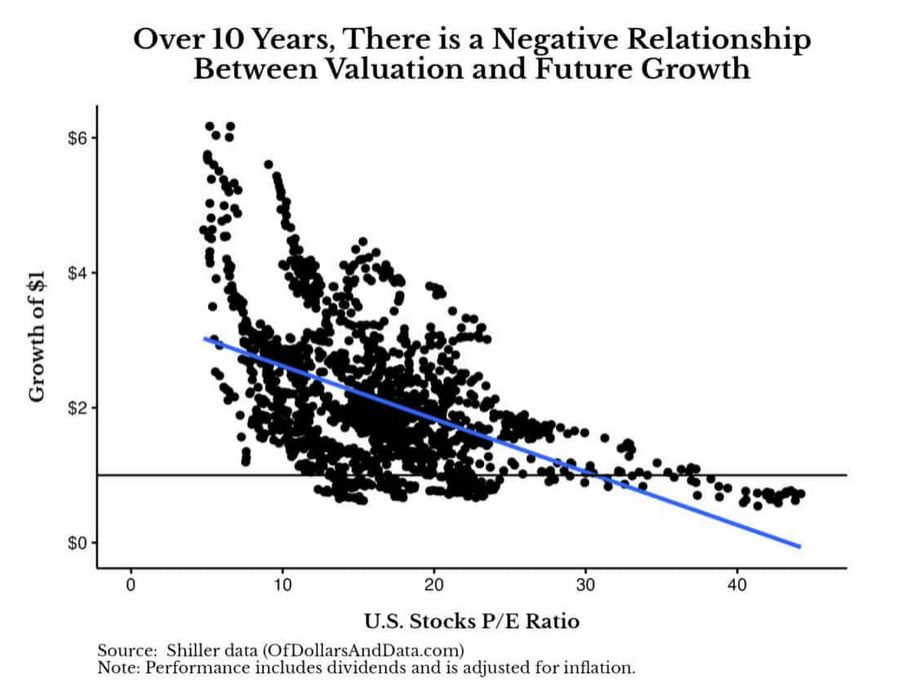

The inverse correlation between Shiller PE and future 10 year returns

Now look at the chart below that has analysed historical data showing the growth of $1 (on the y-axis) over the next 10 years based on the Shiller PE ratio at which one started investing. (on the x-axis) The diagonal blue line shows clearly that as valuations increase, the next 10 year returns decrease.

So with the Shiller PE currently hovering at 41.87, and if historical data is anything to go by, returns projected over the next 10 years are near zero as you can see from the chart.

The above data seems to suggest that if one invests in the US market today, one should be cautious and have tempered or low expectations of future returns.

Note: I am not for a moment suggesting that diversifying your portfolio to include or add US equity is not a good idea. International diversification is certainly a very important part of one’s investment strategy and the US has historically certainly been one of the best performing markets in the world. So an allocation to the US markets is certainly both a valuable & valid diversification for most investors over the long term. In fact, my own portfolio is diversified and includes meaningful exposure to the US. However, given sky-high valuations of the US market (second or almost equal to the dot come bubble) one needs to temper one’s expectations of future returns from the US market.

Risk of going down the GIFT city route

Added to the above returns expectations, there’s another angle that Indians investing currently from India have to factor into investing in the US equity markets have to take into consideration. And that is the risk of not being able to invest relatively small SIP like amounts into the US market.

Since the RBI has capped the amount that Indian MFs can invest in foreign markets, most regular MFs are closed for fresh investments or at least the choice of funds has narrowed significantly.

On the other hand, if one chooses to circumvent this by investing via GIFT City, the issue is that most GIFT city funds require a minimum of USD 5000 i.e. nearly 5 lakhs. By being forced to invest 5 lakhs at a time & not being able to do SIPs for smaller amounts you are effectively being forced to invest very large sums into a market at an all time high since 1880s. That’s not a very good situation to be in at all.

Summary & solution

In summary, from a long term perspective, having some asset allocation to the US equity markets is always a good idea given it’s long term track record. However, given that the US markets are at their second highest valuation since the 1880s – second only to valuations prior to the dot com crash – one must be prepared for relatively low returns form the US over the next 10 years. There exists one more risk that Indian investors should be aware of. That is the fact that investing via the GIFT city route requires a minimum of nearly 5 lakhs. This means that you cannot invest small typical SIP like sums over a long time period. This increases the risk that a large chunk of your money might get invested at an all time high & crash thereafter.

Disclaimer: I am not a financial advisor. My articles are meant for people who are not savvy or well versed with personal finance and investing and find it difficult to grasp all the jargon typically used when discussing such topics. I hope to be able to demystify investing and make it as simple as possible for everyone. I’ve invested in Mutual funds for approx. 24 years. I’ve also been a diligent student of the subject of investing over the past 24 years learning & applying the writings of luminaries in the field. In these articles I’m merely sharing my experience & learning from that investing journey and the books of luminaries in the field in the hope that it might help others in some way. I am in no way directly or indirectly claiming to be a hot shot investor who has generated exceptional or even above average returns during my investment journey. However, I am quite confident that even if all you do is learn from my mistakes, educate yourself on sound investment principles & develop good financial habits you will benefit greatly. Please ensure that you consult a financial advisor before taking any decisions or actions concerning your personal finances or investments. I shall not be liable.

Credits: Nick Maggiulli https://ofdollarsanddata.com/