Key takeaways:

- Everyone knows we should buy when prices fall but not many know HOW MUCH more to buy when markets do fall because markets could keep falling for an indefinite period in the future

- This article presents Dr. Bill Bernstein’s guidelines / thumb rules for this

- Dr. Bernstein is co-founder of Efficient Frontier Advisors, ($ 25Mn min investment) has authored over 10 books on investing and his insights are sought after by the world’s leading financial media

- During market crashes / dips, Dr. Bernstein suggests you increase your allocation by one fifth (or 20%) of the extent of the fall

- During market bubbles, Dr. Bernstein suggests you decrease your allocation by one tenth (or 10%) of the extent of the rise

- Caution: This technique should only be used by very seasoned or experienced investors

Everyone understands the concept of “buying the dip” and wants to profit from it. But how much should you buy when the market seems to be in a dip? The answer to this question is very elusive and I could not find one for many years but here it is.

I found the answer to the above question in Dr. Bill Bernstein’s thumb rules for buying the dip. In conventional financial terminology, this is an investing concept called Dynamic Asset allocation. i.e. changing your asset allocation based on market valuation

Note of caution: The above dynamic asset allocation approach is recommended ONLY for very seasoned or experienced investors.

Who is Dr. Bernstein & what is his thumb rule for buying the dip?

Dr. William Bernstein, co-founded investment firm Efficient Frontier Advisors. To be able to engage his firm, one needs a minimum investment of $25 Million. For those of us who don’t have $25 million, he has written over 10 books on the subject of personal finance & investing. 😊 He is also frequently interviewed by media houses such as CNBC. His insights have been featured in major financial publications such as The Wall Street Journal, Morningstar, and the Financial Times.

In his book, The Four Pillars of Investing Dr. Bernstein says “You should increase your stock allocation only by very small amounts – say by 5% after a fall of 25% in prices – so as to avoid running out of cash and risking complete demoralization in the event of a 1930s style bear market.” i.e. you increase your allocation by one fifth (or 20%) of the extent of the fall

An example with calculations to explain

Let me try to explain the above with a simple example:

Let’s assume that you have chosen to have an equally balanced 50:50 equity to debt asset allocation

Let’s assume that the markets have fallen by 50% in a 2008 global financial crisis type market crash. So when you review your portfolio during the downturn you find that your allocation of 50% equity has fallen by 0.5 X 50 = 25% to 25% equity.

Example of Market dip / correction

Fall = 50%

One fifth of fall (per Bernstein’s thumb rule) = 10%

So I need to increase my equity allocation by 10%

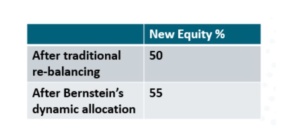

Now my original equity allocation was 50%. Since 10% of 50 is 5%, I need to increase my equity allocation from 50% to 55%..

In the pure re-balancing approach, you would take it back up to 50:50. i.e. you would add 25% to equity to go back from 25% to 50%

But if you were to use Bernstein’s dynamic asset allocation thumb rule you would add a total of 30% to take your allocation back up from 25% up to 55%

Variation in thumb rule for selling during market highs

When I asked Dr. Bernstein about this a while back, he said he still believed the thumb rule applied. The only variation he suggested was that he would rather use a more conservative 1:10 ratio (rather than the 1:5 ratio during a downturn) if one is selling during a market bubble.

Disclaimer: I am not a financial advisor. My articles are meant for people who are not savvy or well versed with personal finance and investing and find it difficult to grasp all the jargon typically used when discussing such topics. I hope to be able to demystify investing and make it as simple as possible for everyone. I’ve invested in Mutual funds for approx. 24 years. I’ve also been a diligent student of the subject of investing over the past 24 years learning & applying the writings of luminaries in the field. In these articles I’m merely sharing my experience & learning from that investing journey and the books of luminaries in the field in the hope that it might help others in some way. I am in no way directly or indirectly claiming to be a hot shot investor who has generated exceptional or even above average returns during my investment journey. However, I am quite confident that even if all you do is learn from my mistakes, educate yourself on sound investment principles & develop good financial habits you will benefit greatly. Please ensure that you consult a financial advisor before taking any decisions or actions concerning your personal finances or investments. I shall not be liable.