Key takeaways

-

The 4% rule comes from back testing based on US data for 50 years

-

Equity & debt returns in India have been falling over the past decades

-

The 4% withdrawal rate was based on the worst period of 30 years from 1926 to 1976

-

Kitces’ research has found a strong correlation between inflation adjusted returns of the first 15-years of retirement and the safe withdrawal rate

-

Kitces’ research shows that during this worst period, the inflation adjusted returns of the portfolio during it’s first 15 years were 0.86%

-

In summary, the 4% rule works as long as the inflation adjusted (real) returns from your portfolio are higher than 0.86% for the first 15 years of retirement

-

Given the reality falling returns, one might want to consider a higher allocation to equity

What is the concern people might have?

The amount one needs to accumulate for retirement or, put another way, the amount one can safely spend / withdraw in retirement is directly determined by the 4% rule. As you can see, it’s therefore a cornerstone for retirement planning.

Some people have voiced concerns that the 4% rule would not work in India because returns in India going forward are likely to be lower. On the face of it, this sounds like a valid concern or argument. However, to check if this is really true, one needs to dig deeper into the origins & basis of the 4% rule.

This article addresses the above concern / question. Let’s start with a recap of the 4% rule.

What is the 4% rule

The 4% rule states that if you withdraw 4% of your retirement corpus on day one of retirement and then in subsequent years adjust that first year amount upwards for inflation, you will most likely not run out of money for 30 years of retirement.

Important caveats to the 4% rule to be noted are:

-

You must have an equity allocation of at least 50%

-

Zero advisor fees AND expense ratios were assumed (i.e. ideally you need to be primarily invested in Direct Index funds)

-

Annual portfolio re-balancing was assumed

-

Intermediate term bonds (between 5 to 10 year maturity) were used

What was the 4% rule based on?

He came up with the above rule by back testing this based on US stock market & bond data for 50 years from 1926 to 1976.

Concern 1: Is the 4% rule valid for India?

Naturally the immediate concern or question that would come up is whether this rule would apply in the context of the Indian equity markets. I’ve attempted to address this in my earlier article here on Whether the 4% rule applies in India.

Concern 2: Will lower returns in future affect the 4% rule?

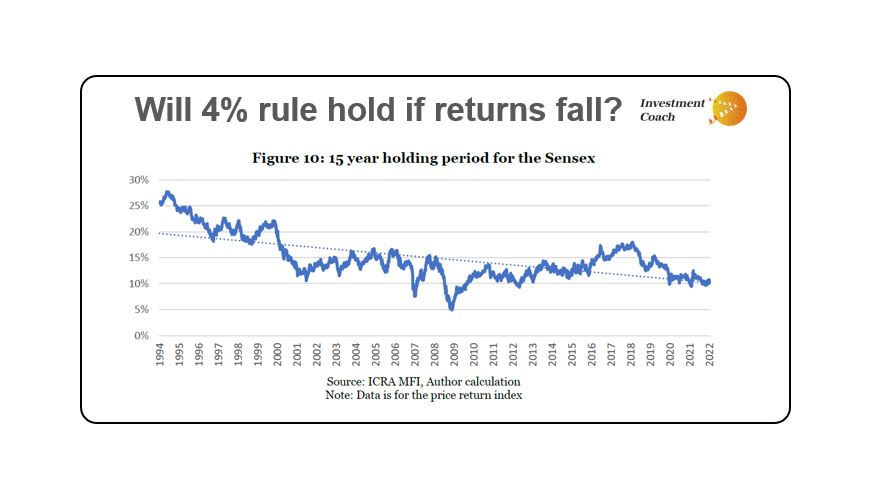

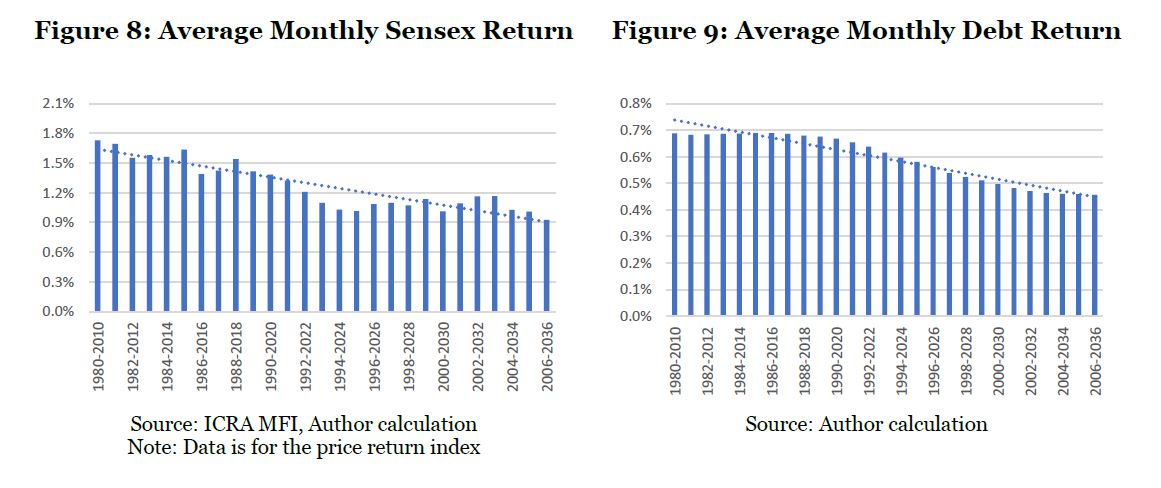

It is indeed true that equity returns in India have been falling over the past decades. See data below compiled by Ravi Saraogi.

Seeing such falling returns data, it would be natural for someone to question whether the 4% rule would still be applicable.

I summarie below research that Michael Kitces has done on this topic to help address the above concern.

Core of the origin of the 4% rule – worst 30-year return

Here is a key point one needs to note very carefully.

The 4% historical safe withdrawal rate was based on the worst period of 30 years from 1926 to 1976.

See the chart below where a retirement period starting 1966 in the US is highlighted. So that was the only year in a 50-year period from 1926 to 1976 that retirees had to reduce spends to 4%. All other years were higher.

Strong correlation between 15-year inflation adjusted returns & SWR

Further, Michael Kitces’ research has shown that there is a strong correlation between inflation adjusted (real) portfolio returns over the first 15 years of retirement and the safe withdrawal rate.

in fact, his research has shown that the 15-year real (inflation-adjusted) portfolio return during the first 15 years of retirement actually has 0.91 correlation to the safe withdrawal rate, as shown in the graph below.

Portfolio returns that generated the worst-case scenario

Now that we have both the above insights, we are ready to dive into the final analysis that will give us the answer to the concern of this article. i.e. whether lower returns will affect the 4% rule for retirement or not.

Kitces analysed the returns during the worst retirement period in US history i.e. the 30-year period starting 1966.

Kitces found that during this worst period, the inflation adjusted returns of the portfolio during it’s first 15 years were 0.86%.

The final answer

The above data point then gives us the final answer. The 4% rule applies, is valid and works as long as the inflation adjusted (real) returns from your portfolio are higher than 0.86% for the first 15 years of retirement. It will not work if returns going forward are so low that you can’t generate even 0.86% above the inflation rate.

This is just one of many reasons why you should measure the returns of your ENTIRE portfolio against inflation about once a year.

It is equally important to measure your personal inflation rate once a year.

So what do you think? Will a mixed portfolio of equity & debt in India manage to generate more than 0.86% over a 15 year period?

One possible way to address the issue

Given the below long-term data from Ravi Saraogi’s paper, we can see that 15 year returns of the Sensex have started to fall to around 10%, it might be prudent to have an asset allocation of at least 60% equity.

Disclaimer: I am not a financial advisor. My articles are meant for people who are not savvy or well versed with personal finance and investing and find it difficult to grasp all the jargon typically used when discussing such topics. I hope to be able to demystify investing and make it as simple as possible for everyone. I’ve invested in Mutual funds for approx. 24 years. I’ve also been a diligent student of the subject of investing over the past 24 years learning & applying the writings of luminaries in the field. In these articles I’m merely sharing my experience & learning from that investing journey and the books of luminaries in the field in the hope that it might help others in some way. I am in no way directly or indirectly claiming to be a hot shot investor who has generated exceptional or even above average returns during my investment journey. However, I am quite confident that even if all you do is learn from my mistakes, educate yourself on sound investment principles & develop good financial habits you will benefit greatly. Please ensure that you consult a financial advisor before taking any decisions or actions concerning your personal finances or investments. I shall not be liable.

Credits: Michael Kitces & Ravi Saraogi